Antitrust regulators should block natural monopolies from acquiring their biggest threats: new potential monopolies

“All happy companies are different: each one earns a monopoly by solving a unique problem. All failed companies are the same: they failed to escape competition.”

— Excerpt from Zero to One, by Peter Thiel

Against all odds, the companies that comprise Big Tech — Facebook, Google, Amazon, and the like — have become villains.

Most ideas about how to address the issues for which they’re being blamed — rampant online abuse, the mishandling of user data, radicalization of both individuals and groups along the political spectrum, and the erosion of democracy — have focused on reintroducing them to competition by breaking them up.

At first glance, this idea makes sense. Competition is the process by which the best companies win by maximizing consumer welfare, and sits at the core of our market economy.

Historically, American antitrust regulators have measured consumer welfare by the relative price of the goods they purchase. This is why companies like Facebook, Google, and Amazon have thus far avoided antitrust scrutiny.These companies are unlike monopolies of yesteryear, which used their market power to force consumers into paying high prices for subpar products.Instead, these new monopolies succeed because people like using their services more than any other one that does what they do, and pay little to nothing for the privilege.

This begs the question: If Big Tech’s ability to thrill consumers is even partially attributable to the companies that comprise it having achieved monopoly status, is breaking those companies up really the best way to go about solving the issues for which they’re being blamed?

The answer, perhaps appropriately, is that it depends. The better question, though, is this: What effect will forced competition have on companies whose business models rely on collecting user data and selling the ability to target users based on it, or companies operating in markets that naturally lend themselves to monopoly?

Fortunately, we don’t have to force companies that have transcended competition back into it to answer this question. History is filled with relevant anecdotes.

For years, the tech industry was rife with companies whose business models forced them into cutthroat competition with one another over user data. These companies then turned around and sold interested parties the ability to target those users based on the data they captured.

This competition should’ve improved the experience of both those interested in capturing attention or selling a product and people using the internet to seek out information in the self-reinforcing cycle tech analyst Ben Thompson calls “Aggregation Theory.”

This did end up happening, but not before a lot of other stuff did.

The initial fever pitch of competition within the search market was, by today’s standards, an unmitigated disaster. Consumers were subjected to search engine experiences rife with clickbait and intrusive advertising. Similarly, scores of companies essentially made up data on the quality of their product or what exactly their data could tell you, screwing advertisers out of money. This contributed to the eventual collapse of the first dot-com bubble, after which AOL spent four years in court fighting its way through lawsuits alleging massive amounts of corporate fraud. Countless firms likely got away with similar behavior.

A logical response to reading this would be to argue that it was greed, not competition, that gave way to this behavior. Put another way, even if AOL had been the only search-based firm in the market at the time, they still would’ve behaved as they did simply by nature of wanting to make as much money as possible. And while this argument isn’t wrong, it misunderstands that greed is both inevitable and harnessable as a force for good. The genius of competitive markets is that by anticipating greed, they’re able to direct it to make everyone better off.

Consider the famous Adam Smith quote:

“It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own interest.”

The same is not true, however, in markets that lend themselves to monopoly, like the ones in which Google and Facebook operate.

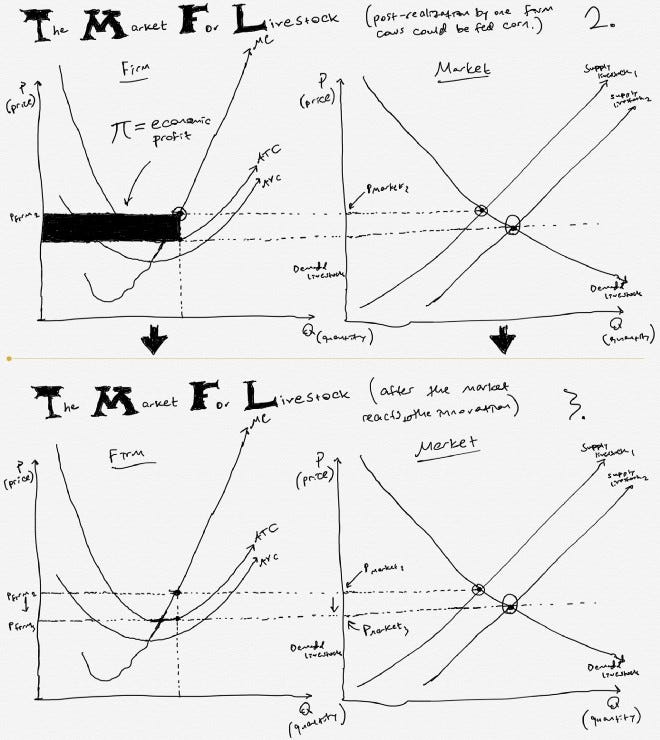

Consider, as a relevant anecdote, the market for livestock.

Because the market for livestock lends itself to competition, we can safely assume two things: first, there are many players, and second, all of them, per greed’s inevitability, are trying to maximize their profits. Thus, they compete to make their product less expensive without sacrificing quality. This includes feeding livestock corn, giving them antibiotics, restricting their movement, separating them from their young — the list goes on.

For consumers, this is (probably) good; we pay lower prices for meat than we otherwise would, and its quality is better than it would be in, say, a developing nation, where competition is nonexistent.

But the relevance of this anecdote is that in the situation we’re describing, we’re no longer the consumer of the product. Instead, we’re the commodity tech platforms are competing to harvest. In other words, we are the livestock.

Understanding tech companies’ models from this perspective makes it clear that the best possible situation for us, as it would be for the livestock, is one in which a single firm comes to dominate the market. This would give said firm the ability to set prices, which would free them — and whatever product they’re selling — from the constraints of all they currently do to keep prices low.

Now, because the market for livestock does not lend itself naturally to monopoly, it’s unlikely that any one player would ever dominate it. More likely would be that consumer tastes would evolve via consumption of propaganda illustrating how poorly livestock are treated (see: Food, Inc.). As this occurred, food conglomerates would be forced to either reexamine their practices or lose out on business.

The situation with data-driven companies, however, is different.

What occurred with AOL in the early 2000s is the price we pay for the emergence of an eventual monopoly, like Google, whose functionality dwarfs those of its now-defunct competitors. Crucial to understand, too, is that it was precisely the failures of competitors like AOL that taught Google what it would take to earn not just the attention, but the adoration of people; or what it would take to earn the monopoly it did.

The takeaway here isn’t that we eliminate competition entirely, like what happens in the pharmaceutical industry when companies are granted patents to develop drugs. Rather, it’s that once a company in a market that lends itself naturally to monopoly emerges from competition to dominate the market, we should celebrate it, not vilify it. Transcending competition marks the first moment the company can begin focusing primarily on its value to the people that use it, as opposed to the day-to-day fight for survival.

As Silicon Valley investor and founder of PayPal Peter Thiel notes in his book, Zero to One:

“In business, money is either an important thing or it is everything. Monopolists can afford to think about other things than making money; non-monopolists can’t. In perfect competition, a business is so focused on today’s margins that it can’t possibly plan for a long-term future. Only one thing can allow a business to transcend the daily brute struggle for survival: monopoly profits.”

Of course, plenty of people remain unsatisfied with platforms that have “escaped competition,” like Facebook. But the point above should make it clear that more direct competition — i.e., Facebook 2.0 — is not what Facebook needs. As we’ve seen with AOL, competition along the same vectors in industries that lend themselves naturally to monopoly, while an effective means, is not a worthwhile end.

Further, claiming that more direct competition for Facebook will solve its problems is to ignore what makes social media outlets valuable in the first place. Google could come out with a new social network tomorrow — call it “Google++” — that was better than Facebook in every way. But if no one joins the network, it’s useless. And given the head start Facebook has, it’s unlikely anyone will.

Now, you could look at this and say, “Well, that’s unfair because it stifles competition.” But is this really the case? There are plenty of new social networks and platforms that have emerged over the past few years. All of these platforms, however, have succeeded precisely by avoiding competition with Facebook and Google.

The world as it exists now is filled with industries dominated by companies who succeeded by drawing finish lines only they could see, then crossing them just as it was becoming clear to everyone else that they even existed. In this world, the only way to compete is by running a different race.

As an example of a company doing so, take TikTok.

TikTok launched in September of 2016 and has grown massively since, adding 75 million users in December of 2018 alone. The app now counts 500 million users globally, with roughly 27 million of those users based in the United States.

TikTok is popular because it baked a functionality into its app that no other app had, or if they did, said functionality wasn’t nearly as built out or useful as TikTok’s. Still, while this functionality explains the app’s initial popularity, the reason TikTok remains popular is twofold: first, every additional person that joins the app increases its value to existing users, and second, each additional person that joins TikTok, as with any social network, makes prospective users marginally more likely to choose it over a competitor.

This, again, is why it doesn’t make sense to say that social networks should be forced to compete over us on the same vectors — that is, once a network has transcended the initial competition that inevitably exists in all of them.

If there is a world with many different social networks or platforms that improve exponentially as more people use them, it will only be because each platform has a specialty the others don’t. In other words, a world of many useful social networks/platforms is one in which all of them have outcompeted the now-defunct upstarts that once vied for monopoly status in their specific vector.¹

The companies that escape this competition are the ones that can now focus on boosting their specific value proposition, as opposed to scrapping for ad dollars to stay afloat.

This gets at the only prescriptive statement I’ll make in this piece, and it isn’t a new idea: that is, no company operating in a market that lends itself to monopoly should be allowed to acquire another unless the two companies have the same value proposition. That means that Facebook never should’ve been allowed to purchase Instagram or WhatsApp, but purchasing MySpace would’ve been fine.²

Consider why this makes sense. Facebook and MySpace’s value propositions to consumers were virtually identical: both networks were places where your friends were, allowing you to replicate your real-life “social network” on the internet. Unless one of these networks had tweaked their value proposition, only one of these companies was ever going to dominate.

That company turned out to be Facebook.

As Facebook added more users, it became marginally more useful to new ones, which caused it to grow exponentially. This also made it a relatively more attractive destination for advertisers looking to target users.³ Capitalizing on demand for their users’ attention turned Facebook into a cash cow, and gave them the resources to continue investing into their platform. This effectively guaranteed they’d remain superior to any direct competitor.

But that’s just it: Instagram and WhatsApp, and for that matter, Snapchat, weren’t direct competitors — and that was exactly what made them threats.

Both could only really be considered competitors to Facebook in that time spent on them (pre-Facebook acquisition) was time not spent on Facebook. Competition in monopolistic markets, however, isn’t the same as competition within competitive markets — and the distinction is crucial.

In naturally competitive markets, like the market for livestock, many firms offer an undifferentiated commodity at the same price. This goes on until one firm discovers an innovation that allows them to undercut that price — like realizing cows could eat corn — and briefly captures an outsized portion of market share. This is known as an economic profit and typically lasts for a brief period before companies gain access to the same innovation. These companies then flood the market with the product, lowering their price, and eventually eliminating all economic profits in the market.⁴

Competition within a naturally monopolistic market, however, is different. It exists at the beginning, yes, and vitally so; initial competition in every market benefits consumers in the long run, acting as a stress test that finds and exposes any possible weaknesses of the competing firms. But the only reason competition within a market that lends itself naturally to monopoly benefits consumers is because eventually — i.e., in the long run — one firm wins that competition (and, inevitably, countless others lose).

Competition within a market that lends itself to monopoly, then — by definition — does not exist.

It follows that since a true monopoly has no competition, the only thing capable of threatening it is another monopoly with the capability to render it not so much obsolete, but irrelevant. This is what Instagram, WhatsApp, and Snapchat all had the potential to be — and do — to Facebook.

This explains why Facebook was so keen on acquiring all three, even as the sums for the two it ended up getting seemed absurd at the time: $1 billion for Instagram — which, in 2012, had 13 employees, 27 million users, and zero revenue — and $22 billion for WhatsApp, which, in 2014, had 55 employees, 420 million users, and also zero revenue.

This also sheds light on what is possibly the only sensible regulation surrounding these companies. If the goal is limiting their power, the first step is to spin off their acquisitions of any company whose eventual monopoly could’ve posed a threat to their own. Instagram and WhatsApp should be included in this group; Whole Foods should not.

The second step is to stop them from acquiring what cannot accurately be called their competition, but can certainly be considered threats: that is, other potential monopolies. Doing so will ensure that new monopolies have the opportunity to emerge, which is vital; progress, as Thiel notes, is driven better monopoly businesses replacing incumbents.

Consider this quote from tech analyst Ben Thompson in his recent article, “Tech and Antitrust:”

“Instagram bought Facebook another five-to-ten years of dominance. That, though, is itself evidence that social networks are not forever. Each generation has its own preferences, and as long as acquisition rules around network-based companies are significantly beefed up, the best solution for Facebook, at least from an antitrust perspective, is simply time.”

The takeaway here shouldn’t be contrarian, but in our competition-obsessed world, probably is: that is, competition is not always good, and monopolies are not always bad. As seems to always be the case, trying to deal with these issues by painting them as black and white omits the nuance necessary to understand and solve them.

Footnotes:

¹ The human tendency to succumb to survivorship bias, defined as “the logical error of concentrating on the people or things that made it past some selection process and overlooking those that did not, typically because of their lack of visibility,” explains our tendency to ignore all the flaws of the companies who, for one reason or another, failed. Instead, we focus on the flaws of the companies that succeeded, glorifying all their failed competition as we do. I’ve previously written about survivorship bias here, and I recommend looking further into the idea. Once you understand it, your perception of the world shifts.

² Notice that in markets that lend themselves to monopoly, the optimal situation is having only one player in the market. It follows that companies competing in a market that lends itself to monopoly must by definition have virtually identical value propositions — if they don’t, they aren’t competitors. The natural outcome for a market in this situation is either (a) that one acquires the other, or (b) that they merge.

³ Facebook and Google captured 68% of digital advertising spend in the U.S. last year.

⁴ Figure 1 illustrates the market for livestock under perfect competition. Figure 2 illustrates the market for livestock under perfect competition, but one firm has figured out that by feeding cattle corn, he can decrease his costs while still selling his product for the market price. This earns him an economic profit, indicated by the shaded area Figure 2. Figure 3 illustrates the market for livestock after suppliers enter the market to capture some of the economic profit. This lowers the market price to the point that the firm who discovered the innovation is no longer earning an economic profit, indicated by the lack of a shaded area in Figure 3.